How Sale-and-Leaseback Accounting Works in 2024

Accounting for the sale of Leaseback equipment

Sale-and-leaseback transactions have long been popular because they benefit both sellers and lessees. However, in recent years, accounting for such transactions has changed significantly as the FASB has issued new revenue recognition and lease accounting standards.

FASB’s new lease accounting standard makes it less difficult to determine whether control is transferred from a seller-lessee to a buyer-lessor during the construction of an asset. However, applying these provisions can be difficult for creators of organizations with complex lease agreements.

The FASB Leases Accounting Standard (FASB ASC Topic 842, Leases) issued in 2016 requires a lessee to record right-of-use assets and related obligations in connection with operating his leases with terms exceeding 12 months. That is what is required. Under previous guidance (ASC Topic 840), payments related to operating leases were treated as expenses, so such leases were not recognized on an entity’s balance sheet. The new standard has a superficial impact on lease transactions that previously met the Finance Lease Topic 840 standard. As a result, such leases are renamed finance leases and are classified as intangible rights of use subject to amortization under current guidance. On the lessor side of these transactions, the lease classification standards have changed, but the new standards provide for the same lease classifications: operating leases, direct financing, and sales leases. Additionally, the lessor party’s accounting for these transactions will be affected by new revenue recognition principles codified in ASC Topic 606, Revenue from Contracts with Customers.

Nature of Leaseback:

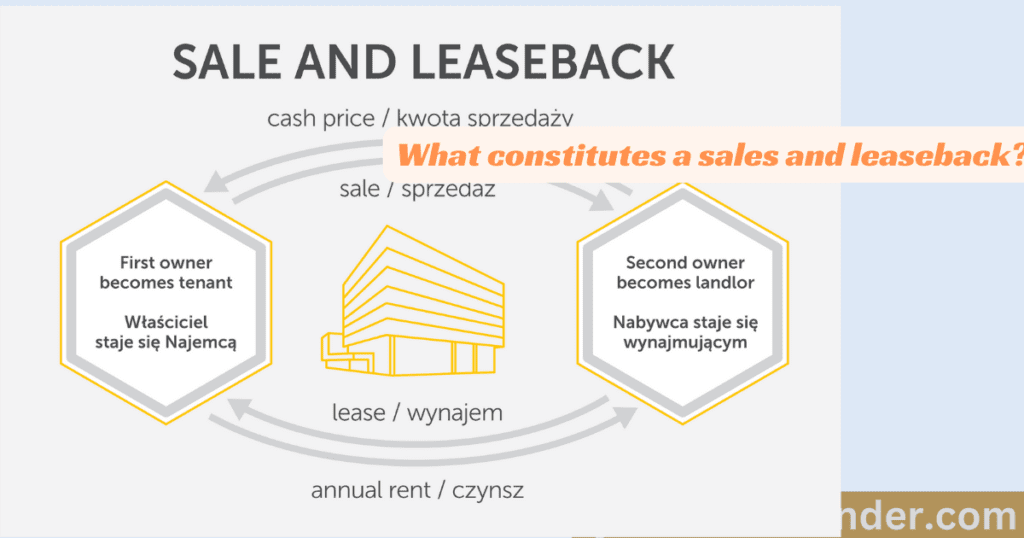

A sale and leaseback, or more simply a leaseback, is a contract between a seller and a buyer in which the former sells an asset to the latter and then sells that asset to the latter. Enter into a second leaseback agreement. Benefits for the buyer as a seller-lessee include:

An immediate inflow of funds that can be used in a particular line of business of a company.

A more advantageous form of financing because it allows parties to structure transactions to reduce the costs of traditional financing (such as collateral, credit covenant violations, closing costs, and the possibility or limitations of balloon payments).

- Benefits for the buyer-lessor through leaseback include:

- Direct confirmation of the creditworthiness of the seller-borrower reduces the risk of default.

- Possibility to exit the contract more easily than with traditional financing.

- Important Tax Benefits – Depreciation Expenses. and

- Residual Value Guarantee at Termination.

Despite the challenges of implementing Topic 842’s detailed reporting and disclosure requirements, leasebacks will continue to be a popular vehicle for both parties due to the benefits derived from this funding source.

What constitutes a sales and leaseback?

The debate as to whether a transaction qualifies as a sale and leaseback transaction depends on the relationship between the seller and lessee and whether control is transferred to the buyer-lessor. To achieve control, a sale must comply with the requirements of Topic 606, specifically paragraphs 606-10-25-1 through 606-10-25-8. These paragraphs determine whether a contract exists. Article 606-10-25-30 governs whether a performance obligation is satisfied. However, compliance with these provisions alone is not sufficient to ensure a successful transfer of control and a successful leaseback. The transaction should result in operating lease classification for the seller-lessee. None of the criteria in Section 842-10-25-2 for recognition as a finance lease may exist. If any of the criteria in this paragraph are met, control of the underlying asset is not considered a valid transfer, the seller-lessee must classify the transaction as a finance lease, and the proceeds of the sale must be treated as a loan. The criteria underlying classifying a transaction as a finance lease are:

When the lease ends, ownership of the asset is transferred to the lessee.

A lessee has an option to purchase an asset that is reasonably certain to be exercised.

The lease term represents the majority of the remaining useful life of the asset.

The present value of the sum of the lease payments and the residual value guaranteed by the lessee must be substantially equal to or greater than the total fair value of the underlying asset. and

The underlying asset is special and must exclude alternative uses by the lessor at the end of the lease term.

Additionally, according to Section 842-40-25-3, virtually any option by a seller-borrower to repurchase an asset is subject to the terms and conditions of the seller-borrower unless the option is at fair value and the asset in question is a commodity in nature. , preventing it from being treated as a sale.

Successful Sale and Leaseback Example:

Assume the following information.

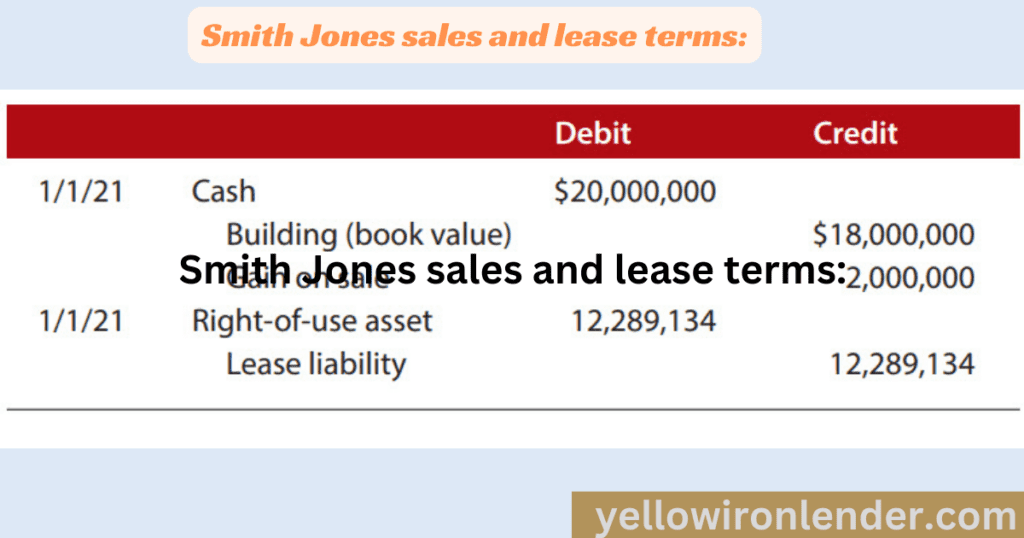

Cash Shortage, Smith Corp. Jones Co. and Alliance agreed to sell the building used for business and then entered into an agreement with Jones to lease the building back from Jones, which would allow Smith to continue to use the building. (See Smith Jones Sales and Disposals table). ).

Smith Jones sales and lease terms:

The seller-tenant evaluates the sale following Sections 606-10-25-1 through 606-10-25-8 and Section 606-10-25-30 and determines that the transaction is a Topic 606 sale. Decide. Next: Based on the information in the Smith-Jones sales and lease term sheet, sellers and lessees evaluate the lease classification criteria in paragraph 842-10-25-2. There is no transfer of ownership. This means that after the transfer, ownership remains with the buyer–lender, and no purchase or renewal options are available to the seller-borrower.

The rental period is only 33% of the building’s remaining useful life. The present value of the lease payments is $12,289,134 ÷ $20,000,000, representing just over 61% of the fair value of the asset. And the assets are not unique. Because none of the criteria in Section 842-10-25-2 are met, the seller-lessee may classify the lease as an operating lease and the transaction may qualify as a sale-and-leaseback.

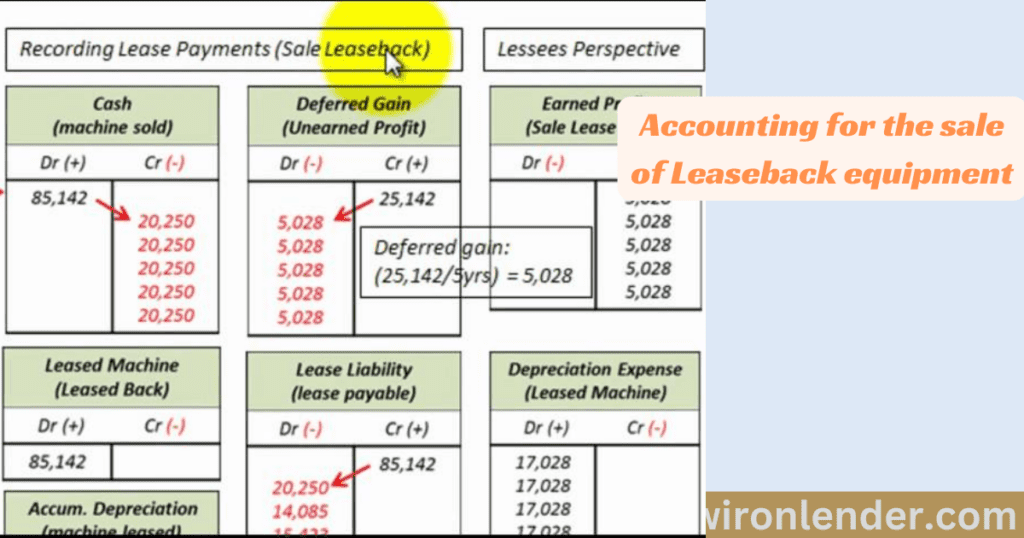

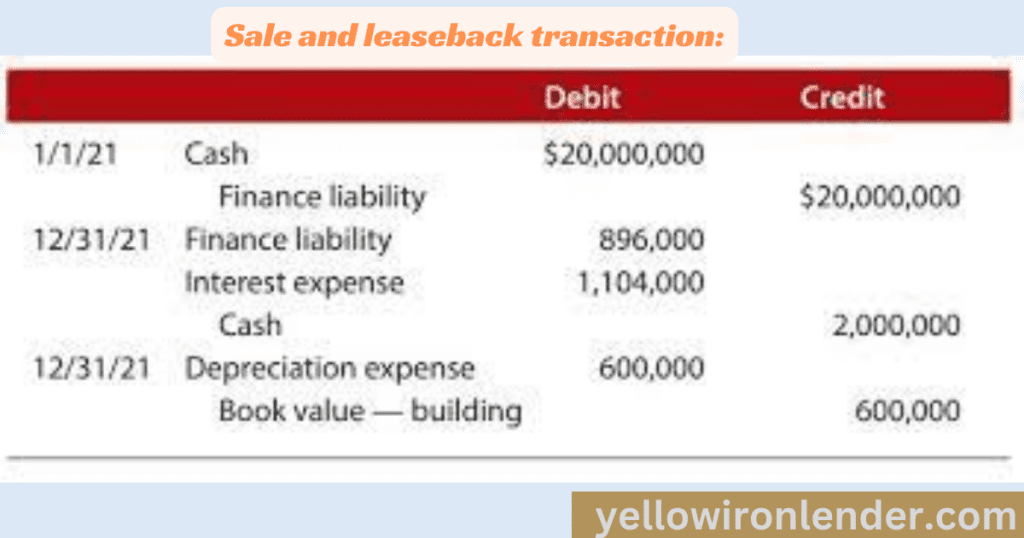

Under these circumstances, the seller-tenant would record cash proceeds of $20,000,000, write off the carrying amount of the building from its books, and record a gain on sale of $2,000,000. Additionally, the seller-lessee would recognize a right-of-use asset and related lease liability of $12,289,134. Based on this information, the seller-lessee prepares the journal entries shown in the sale and leaseback transaction table.

Sale and leaseback transaction:

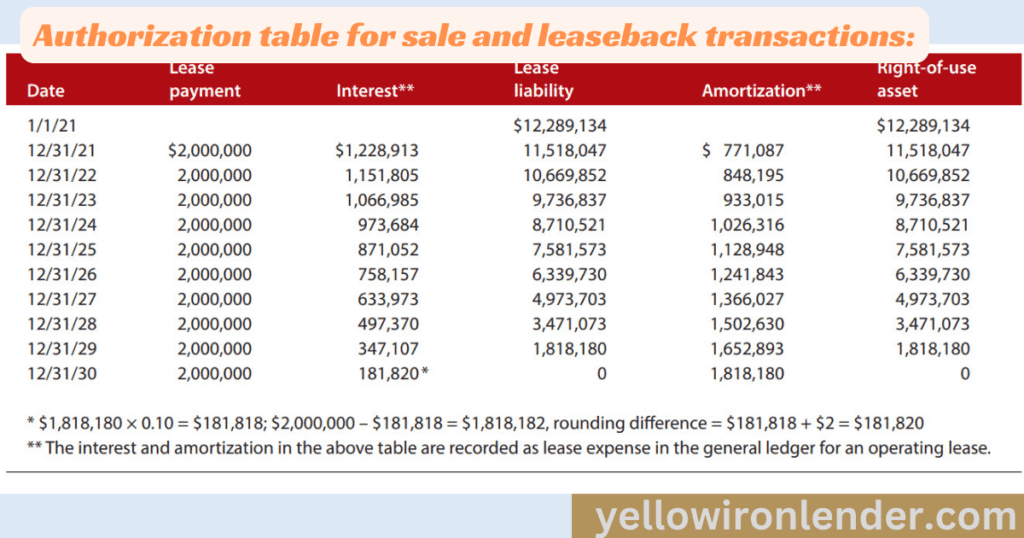

Over the remaining term of the lease, the seller-lessee recognizes lease expense on a straight-line basis. The lease liability is amortized using the effective interest method and the right of use is reduced by the difference between the straight-line rental expense and the reduction in the lease liability. By the end of the lease term, both the lease liability and the right-of-use asset are amortized to zero (assuming no initial direct costs or incentives), as shown in the table Amortization Table for Sale and Leaseback Transactions.

Authorization table for sale and leaseback transactions:

On December 31, 2021, the seller-tenant records the transaction as shown in the “Journal Entries Based on Chart of Amortization” table.

The seller-tenant will make similar entries for the remaining nine years. Now assume that the contractor is his Smith Corp. and has been granted an option to purchase the building on January 1, 2026, for $12 million, and properties similar to the subject property are not readily available on the market. In this case, the transaction cannot yet be considered a successful sale and leaseback.

Journal entry based on Authorization table:

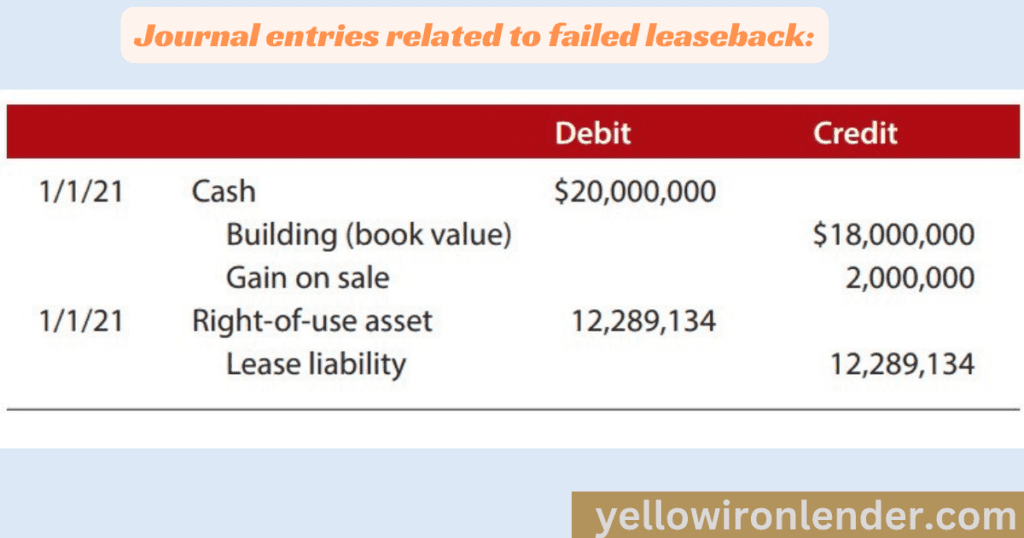

Illustration of failed sale and leaseback:

Smith Corp.’s option to purchase the building at the end of the fifth year causes the transfer of the property to no longer be treated as a sale under section 842-40-25-3 (subject to the narrow exceptions in subparagraphs a and b). is as follows). (not applicable). fulfilled). In this case, the transaction is not considered a sale and leaseback and must be treated as a loan under Section 842-40-25-4. This process recognizes the financial responsibility of the seller-borrower. Additionally, the seller-tenant is not permitted to derecognize the asset and must continue to record depreciation expenses on the building.

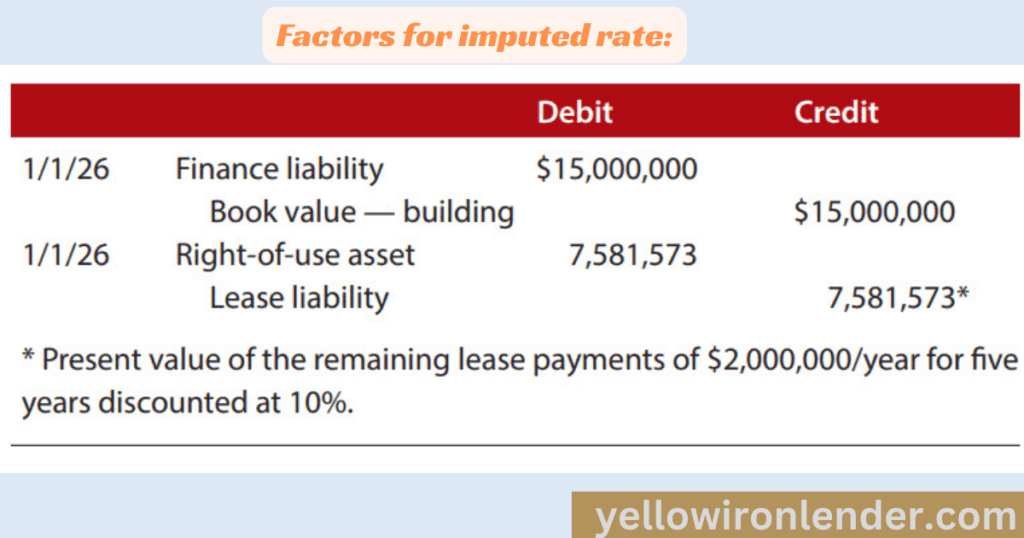

In these situations, Section 842-40-30-6b requires that the carrying amount of the asset shall not exceed the carrying amount of the liability at the end of the lease or when control of the asset is transferred. requesting. The earliest of the buyer’s and landlord’s dates will apply. The seller-tenant must establish an interest rate that corresponds to the carrying amount of the financial liability and the carrying amount of the building at the time the option is exercised. Based on the fact pattern above, this date corresponds to December 31, 2025. The book value of the building on this date is $18 million – ($600,000 × 5) = $15 million. The imputed interest rate is calculated using the numbers in the Imputed Interest Calculation Factors table.

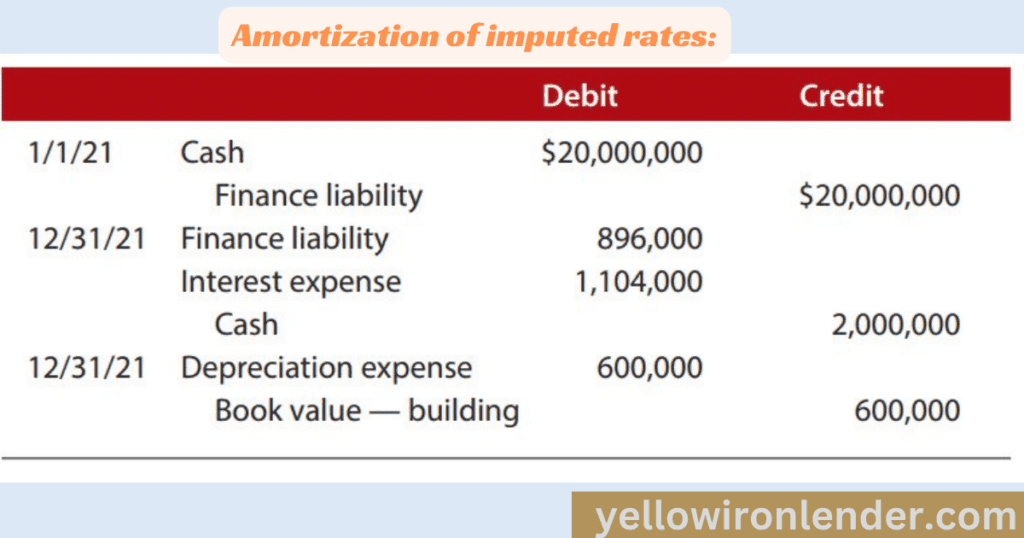

Factors for imputed rate:

Using an imputed interest rate of 5.52%, the amortization schedule would be ‘Amortization at imputed interest’.

Amortization of imputed rates:

In connection with this financing, Smith Corp. records the transactions as shown in the “Journal Entries Related to Failed Leasebacks 2021-2025” table.

Journal entries related to failed leaseback:

Similar entries must be made by December 31, 2025.

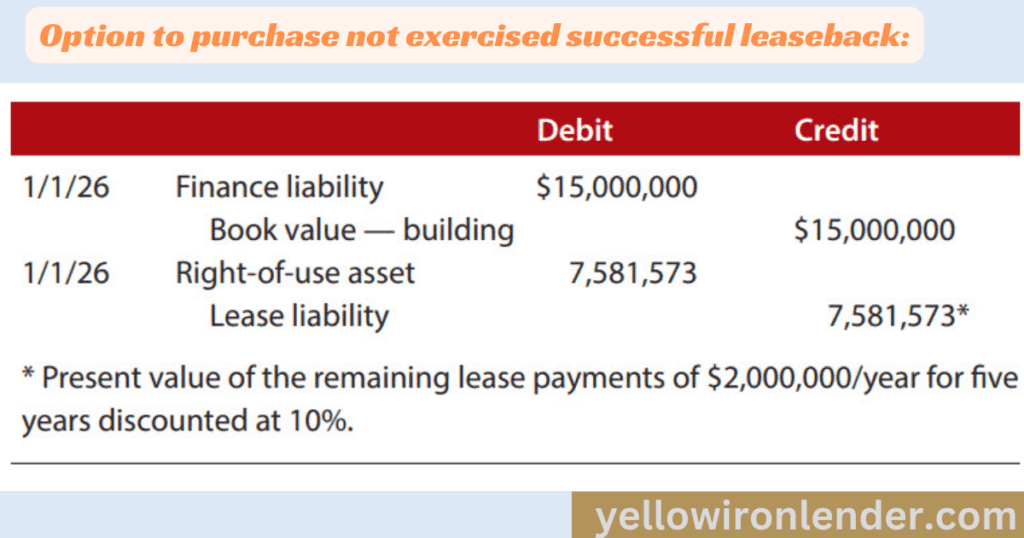

Assume Smith Corp. Does not exercise the option. This lease agreement meets the requirements for classification as an operating lease and treatment as a leaseback. In this case, eliminate the book value and loan liability for the Smith Corp. building. In essence, such an elimination constitutes a sale because the seller tenant is effectively transferring control of the underlying asset (such as the building) to the buyer tenant. The seller-lessee would also record a right-of-use asset and an associated lease liability equal to the present value of the remaining lease payments (2026 to 2030). in January Beginning January 1, 2026, the seller-lessee will make the entry described in the table “Purchase option not exercised: Successful end-of-2025 leaseback justification.”

Option to purchase not exercised successful leaseback:

On December 31, 2026, Seller-Tenant creates the entries listed in the Seller-Tenant Journal Entries table. A similar reservation will be made for the remaining rental period based on the first amortization chart.

Journal entries for seller lessee:

Remaining Challenges:

Looking at examples of sale and leaseback successes and failures, the application of the relevant paragraphs of Topic 842 seems relatively straightforward. However, in many leaseback instances, it is difficult to determine when to control transfers, particularly in real estate transactions where one party sells a building owned on land owned by another party. The previous guidance, Topic 840, made it difficult for many companies to apply the broad provisions and make related disclosures. Here, in paragraphs 842-40-55-40 through 842-40-55-44, the FASB provides the above guidance regarding the criteria underlying whether control is transferred from a seller-borrower to a buyer. We have streamlined the cumbersome provisions of. The lessor in transactions involving assets under construction. Despite the new guidelines, applying these provisions to more complex lease agreements will continue to be a challenge for many businesses.

Deferral of Effective Date:

Due to the coronavirus pandemic, the FASB resolved to defer the effective date of the lease accounting standard for certain entities by one year. With this delay, FASB ASC Topic 842, Leases, becomes effective for private businesses and private nonprofit organizations for fiscal years beginning after December 15, 2021. The effective date is a public non-profit organization that has issued conduit debt or is a debtor whose securities are traded, listed, or offered on a stock exchange or over-the-counter market and has not yet published financial statements. Applies to organizations. These organizations have fiscal years beginning after that. Starting December 15, 2019.

Conclusions:

In conclusion, our exploration of accounting for sale-leaseback equipment illuminates the strategic and financial implications for businesses engaging in this transaction. By delving into the nuances of sale-leaseback arrangements, we’ve uncovered how companies can leverage this financial strategy to unlock capital, enhance liquidity, and optimize their balance sheets.

The accounting intricacies, including recognizing the sale and leaseback elements, present both challenges and opportunities. Properly navigating these complexities is essential for accurate financial reporting and compliance with accounting standards.

As businesses consider sale-leaseback transactions as a means of unlocking the value of their equipment, it becomes apparent that this financial strategy is not only about immediate cash infusion but also about creating flexibility for future growth and operational agility.

In the dynamic landscape of business finance, accounting for sale-leaseback equipment emerges as a tool for financial optimization, allowing companies to allocate resources strategically, improve financial ratios, and strengthen their overall financial health. As organizations continue to seek avenues for capital efficiency, sale-leaseback transactions stand out as a viable and strategic option, providing a pathway to navigate the intricate intersection of accounting, finance, and operational considerations.

FAQs:

How are sales leasebacks accounted for?

Accounting for sale-leasebacks and ASCs 842

Sales and any gains or losses received when the buyer-lessor assumes control of the asset. It shall be recorded as the difference between cash and the carrying amount of the asset.

Derecognize the asset and remove it from the balance sheet.

How do I record leased equipment in accounting?

Once you have gathered the information (that is, you know the lease term, lease payments, and discount rate), simply discount the liability over the lease term using the discount rate. The lease liability or resulting amount is then recorded on the balance sheet. Then record the leased item.

What is equipment sale-leaseback?

Simply put, a sale-leaseback is when we purchase your equipment outright and lease it back directly to you. This gives your business an immediate influx of cash and means you own the equipment again at the end of the period.

What transactions are subject to sale-leaseback accounting?

A sale-leaseback transaction occurs when a company sells an asset it owns and immediately leases that asset back from the buyer. In that case, the seller becomes the lessee and the buyer becomes the lessor. These types of transactions affect the accounting records of both the seller-borrower and the buyer-lender.

Is a sale leaseback a finance lease or an operating lease?

A seller-tenant sells land or buildings and at the same time rents them back from a buyer-tenant. Leasebacks of buildings are classified as finance leases, and leasebacks of land are classified as operating leases.